The Indian insurance industry is undergoing rapid digital transformation, with technology becoming the driving force behind innovation. The rise of InsurTech — a blend of insurance and technology — has reshaped how policies are sold, managed, and claimed.

From personalized digital platforms to AI-powered claim settlements, InsurTech trends India are redefining the customer experience and making insurance more accessible, transparent, and efficient.

What Is InsurTech?

InsurTech refers to the use of technology to improve and simplify insurance services. It includes innovations like mobile-based policy management, data analytics, automation, blockchain, and artificial intelligence that make insurance faster and more customer-centric.

In India, InsurTech startups and established insurers are leveraging these tools to reach underinsured populations and modernize traditional insurance operations.

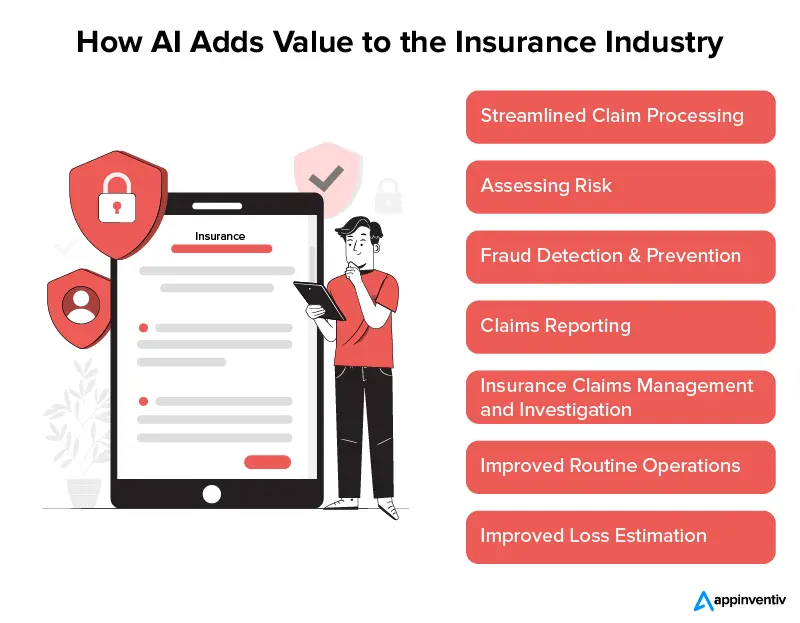

1. Artificial Intelligence and Automation

AI is at the core of the digital insurance revolution. From customer support chatbots to AI-driven underwriting, automation is streamlining every step of the process.

AI helps insurers predict customer needs, detect fraud, and process claims faster — reducing costs and improving customer satisfaction.

2. Usage-Based and On-Demand Insurance

Modern consumers seek flexibility, and usage-based insurance (UBI) is answering that demand. Policies now adapt to how and when people drive, travel, or use gadgets.

“Pay-as-you-drive” car insurance and “trip-based” travel insurance are perfect examples of how InsurTech trends India are redefining coverage models.

3. Blockchain for Transparency

Blockchain technology is enhancing trust between insurers and customers by enabling secure, tamper-proof data sharing. It simplifies claim validation and reduces fraud, ensuring faster settlements and transparent records.

4. Digital Distribution and Embedded Insurance

InsurTech has made buying insurance as easy as shopping online. Digital platforms and apps allow users to compare policies, renew online, and make claims instantly.

Embedded insurance — where protection is automatically included with products like flights, phones, or loans — is also becoming a major trend in India.

5. Predictive Analytics and Big Data

Insurers now use big data and predictive analytics to assess risks more accurately. By analyzing customer behavior, lifestyle, and health data, they can offer more personalized insurance plans at competitive prices.

6. Cloud-Based Solutions

Cloud computing enables insurers to handle massive amounts of data efficiently, support online customer service, and offer remote policy management. It also helps InsurTech companies scale their operations quickly.

7. Cyber Insurance and Data Security

With growing digital adoption comes a rise in cyber risks. InsurTech companies are responding by developing specialized cyber insurance products for individuals and businesses to protect against data breaches, ransomware, and digital fraud.

8. Collaboration Between Insurers and Startups

Traditional insurance providers are partnering with agile InsurTech startups to accelerate innovation. These collaborations combine regulatory experience with technological creativity, resulting in smarter, faster, and more user-friendly solutions.

The Future of InsurTech in India

The future of insurance in India lies in personalization, automation, and digital-first experiences. As regulatory frameworks evolve and technology becomes more affordable, InsurTech adoption will continue to expand across rural and urban markets.

In the coming years, expect AI-driven advisors, instant claims via mobile apps, and even insurance policies tailored through real-time data analytics.

Conclusion

InsurTech trends in India are redefining the way insurers and customers interact. With technology at its core, the industry is becoming more transparent, efficient, and customer-focused.

For both policyholders and insurers, this digital transformation marks a new era of convenience and trust in the insurance ecosystem.