Why Startups Need Insurance in India

Starting a business in India is exciting — full of innovation, ambition, and opportunities. But it’s also a journey filled with risks. From operational challenges to financial uncertainties, startups face several potential threats that can derail their growth.

This is where insurance for startups in India plays a vital role. It acts as a financial safety net, helping founders safeguard their business, assets, employees, and reputation from unforeseen risks.

In India’s growing startup ecosystem, where small decisions can have big financial consequences, having the right insurance coverage ensures your business can recover quickly from unexpected setbacks.

What Is Startup Insurance?

Startup insurance, also known as business insurance, is a package of multiple coverages designed specifically for new and growing businesses. It protects your company from financial losses that could arise from accidents, property damage, lawsuits, data breaches, or employee-related issues.

Unlike traditional business insurance, startup insurance is flexible. You can choose policies that match your company’s size, industry, and risk exposure — ensuring you only pay for what you truly need.

Why Insurance for Startups in India Is Crucial

Many entrepreneurs believe insurance is for large corporations, not new businesses. But in reality, startups are often more vulnerable. Limited resources and cash flow mean that one major loss — like a fire, data breach, or lawsuit — could severely impact operations or even shut down the company.

Here are key reasons why insurance for startups in India is essential:

- Legal Compliance: Some business insurances, like employee coverage, are mandatory under Indian law.

- Risk Management: Protects your startup from financial loss due to property damage, liability, or cyber incidents.

- Investor Confidence: Venture capitalists and angel investors prefer startups that have adequate insurance protection.

- Business Continuity: Helps your business stay afloat even after unexpected disruptions.

- Employee Security: Provides health, accident, or group insurance to attract and retain top talent.

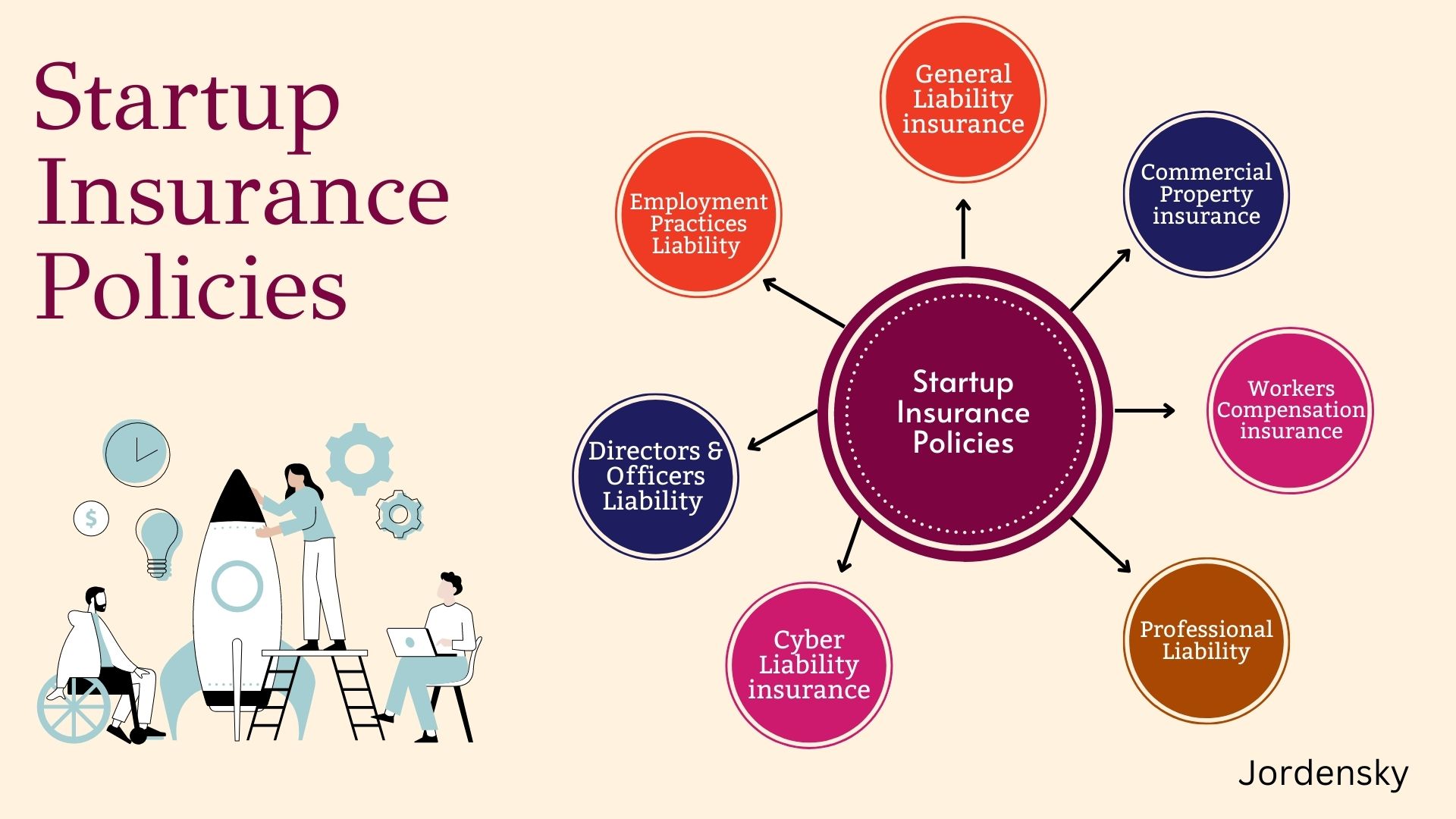

Types of Insurance Every Startup in India Should Have

1. General Liability Insurance

This covers third-party claims for bodily injury, property damage, or personal injury caused by your business operations. For instance, if a client or visitor is injured on your premises, liability insurance helps cover the compensation.

2. Professional Indemnity Insurance

Also known as Errors and Omissions (E&O) insurance, this is essential for tech, consulting, design, or legal startups. It covers legal costs if your professional advice or services cause financial loss to a client.

3. Cyber Liability Insurance

With startups increasingly relying on digital platforms, cyber liability insurance in India protects against data breaches, hacking, and cyber extortion. It covers costs of investigation, notification, and recovery after a cyberattack.

4. Property and Asset Insurance

Protects office equipment, computers, inventory, and furniture from fire, theft, or natural disasters. This ensures your operational assets remain safe even in adverse events.

5. Directors and Officers (D&O) Liability Insurance

D&O insurance protects company founders, directors, and key decision-makers from legal actions arising from their managerial decisions. It’s especially crucial for startups dealing with investors or external stakeholders.

6. Group Health Insurance

Offering health insurance for employees builds trust and loyalty. It also helps startups comply with employee welfare laws while ensuring workers feel protected and valued.

7. Business Interruption Insurance

Covers loss of income if your startup’s operations are interrupted due to a fire, flood, or other insured events. It helps maintain cash flow and pay fixed expenses even when business is temporarily paused.

Benefits of Insurance for Startups in India

- Financial Stability: Shields startups from large, unexpected losses.

- Investor Trust: Many investors require proof of insurance before funding.

- Legal Protection: Covers court costs and settlements in case of lawsuits.

- Reputation Management: Insurance helps recover faster from PR or operational crises.

- Employee Retention: Offering insured benefits improves morale and reduces attrition.

Having these protections in place allows founders to focus on innovation and scaling, without constantly worrying about potential financial pitfalls.

Common Mistakes Startups Make While Choosing Insurance

Even though insurance is crucial, many startups make costly mistakes when buying policies:

- Choosing insufficient coverage to save costs.

- Ignoring cyber and liability risks.

- Not reading exclusions carefully.

- Overlooking the insurer’s claim settlement ratio.

- Not reviewing policies as the company grows.

KaroInsure helps startups avoid these pitfalls by providing transparent comparisons and expert guidance, ensuring you get the best protection for your specific business model.

How KaroInsure Helps Startups Get the Right Coverage

KaroInsure partners with leading IRDAI-approved insurers to make buying business insurance simple and reliable. Whether you’re running a tech startup, food delivery app, or e-commerce platform, KaroInsure offers tailored coverage options.

Here’s how KaroInsure supports startup founders:

- Compare policies from multiple insurers in minutes.

- Get personalized advice based on business type and risk level.

- Transparent premiums with no hidden charges.

- Claim assistance and renewal reminders.

These internal links improve SEO and help readers explore related insurance solutions.

Conclusion: Secure Your Startup’s Future with KaroInsure

The startup journey in India is full of challenges — but with the right insurance, your business can grow fearlessly.

Insurance for startups in India is not just a financial safeguard; it’s a foundation for long-term success. It builds investor trust, protects your employees, and ensures you recover swiftly from any unforeseen event.

With KaroInsure, finding the perfect policy for your startup is easy, transparent, and affordable.

Safeguard your vision, secure your assets, and build confidently — because every great startup deserves reliable protection.