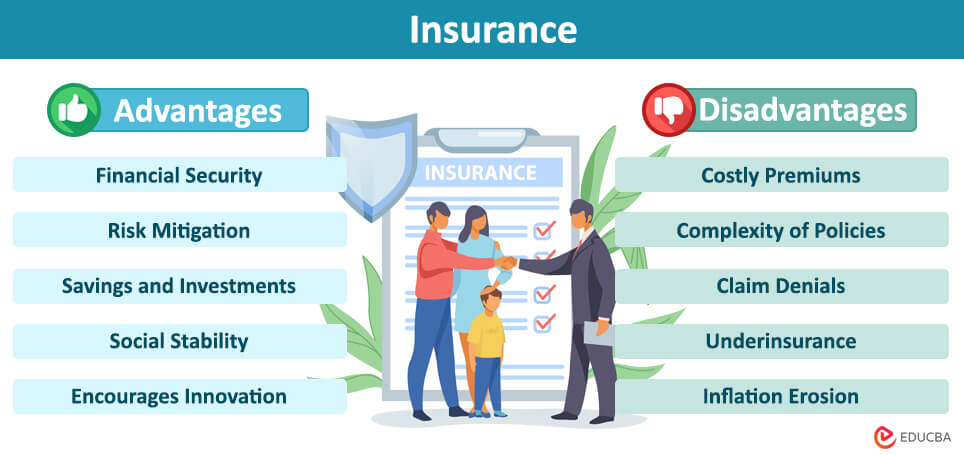

Home insurance offers essential protection for your property and belongings against risks like fire, theft, and natural disasters. Whether you own or rent, this coverage helps safeguard your home and provides financial security in case of damage or loss. With customizable policies, home insurance ensures peace of mind for homeowners and renters alike.

Choosing the right insurance plan is one of the most important financial decisions you’ll make. With so many insurers and options available, it can be confusing to know which policy truly fits your needs. This is where learning how to compare insurance policies the right way becomes essential.

At KaroInsure, we simplify the process—helping you find the best coverage at the most affordable rates. Let’s understand how to make the smartest comparison before you buy.

1. Identify Your Needs First

Before comparing plans, determine what you actually need. Are you looking for health insurance, life coverage, or vehicle protection? Understanding your goals—whether it’s family security, medical care, or financial protection—will help you shortlist only the most relevant options.

2. Check the Coverage Details

Every policy is unique. When you compare insurance policies, pay close attention to:

Sum assured or coverage limit

Inclusions and exclusions

Waiting periods (for health plans)

Policy duration and renewal options

Don’t just go by the price—make sure the coverage aligns with your lifestyle and financial goals.

3. Compare Premiums and Benefits

Price matters, but value matters more. Two plans may offer similar coverage but differ in premium rates and added benefits. Use trusted comparison tools like KaroInsure to see side-by-side differences in:

Premium costs

Rider options (like accidental or critical illness cover)

Claim settlement ratios

This helps you make a fair and informed choice.

4. Review the Claim Settlement Ratio

A policy is only as good as its claims process. Always check the insurer’s claim settlement ratio (CSR)—it indicates how many claims are successfully settled out of total received. A high CSR means greater reliability and smoother claim experiences.

5. Read Customer Reviews and Support Options

Customer feedback offers real insights into an insurer’s reliability. Look for reviews on claim handling, customer service, and online support. KaroInsure partners only with IRDAI-approved insurers known for transparency and customer satisfaction.

6. Use Trusted Platforms Like KaroInsure

At KaroInsure, you can compare insurance policies from top insurers in India—all in one place. Our platform ensures:

Transparent premium breakdowns

Expert advice from certified professionals

Easy-to-understand comparisons

This saves you both time and money.

Conclusion

Comparing insurance policies doesn’t have to be complicated. With the right approach, you can confidently find a plan that fits your needs and budget. In 2025, make smarter financial decisions—compare, understand, and choose the right insurance policy with KaroInsure.

Claim settlement is the process through which an insurance company compensates you or your family for a loss or damage covered under your policy. It’s the most important part of any insurance plan — whether it’s health, motor, or life insurance — because this is when your coverage actually helps you financially.

When you buy insurance through KaroInsure, we ensure that claim settlement is smooth, transparent, and quick, so you can focus on what matters most.

Types of Claim Settlement

There are mainly two ways claims are settled in India:

Cashless Claim – The insurer pays directly to the hospital or repair center.

Reimbursement Claim – You pay first, then submit bills and documents to get reimbursed.

Both processes have their advantages. KaroInsure helps you choose insurers with high claim settlement ratios and simple procedures.

Step-by-Step Guide to Filing a Claim

Here’s a simple process you can follow for a hassle-free claim experience:

Inform your insurer immediately after the incident or hospitalization.

Submit required documents like ID proof, policy details, and bills.

Cooperate with surveyors or inspectors if needed.

Track your claim online through your insurer or KaroInsure’s dashboard.

Receive payment once the claim is approved.

Quick reporting and accurate documentation help speed up the settlement process.

Common Reasons for Claim Rejection

Sometimes claims are delayed or rejected due to small mistakes. Be sure to avoid:

Providing incorrect information during policy purchase.

Missing premium payments.

Failing to submit documents on time.

Filing for non-covered damages.

Always read your policy wording carefully before making a claim.

How KaroInsure Simplifies the Process

With KaroInsure, claim settlement becomes easy and stress-free. Our experts guide you through every step, from claim intimation to documentation and follow-up. We also connect you with insurers who have the highest settlement ratios and strong customer support in India.

We don’t just sell policies — we help you get the benefit when you need it most.

Conclusion

A claim settlement process should never be confusing or delayed. With proper knowledge and support, you can ensure a fast and fair claim experience. KaroInsure stands with you throughout the journey — from policy purchase to final claim approval.

The year 2025 has brought several important reforms in India’s insurance industry. These changes, introduced by the Insurance Regulatory and Development Authority of India (IRDAI), aim to improve transparency, policyholder protection, and operational efficiency. For anyone holding or thinking of buying insurance—especially through brokers like KaroInsure—knowing these reforms is essential. So below, you’ll find a breakdown of what’s changed, how it affects you, and how to benefit.

Key Regulatory Changes

Here are some of the major reforms introduced or proposed by IRDAI in 2025:

Review of the Insurance Act, 1938

IRDAI formed a high-powered committee chaired by former SBI chair Dinesh Khara to review proposed amendments to the Insurance Act. The Times of India+2Financial Express+2

Possible changes include allowing more foreign direct investment (FDI), simplifying regulatory norms, and modernizing oversight. Insurance Business Asia+2ET Now+2

Mandatory Reinsurance Cession

For FY 2025-26, general insurers have to cede 4% of sum insured from each policy to Indian reinsurers (specifically GIC Re). TaxGuru

This includes a broad set of general insurance policies; terrorism and nuclear pool premiums are exempt. TaxGuru

Internal Insurance Ombudsman Scheme

IRDAI has released draft norms mandating insurers to appoint Internal Insurance Ombudsmen (IIOs) for handling policyholder grievances up to ₹50 lakh. The Economic Times+1

This aims to streamline complaint resolution before escalation to external ombudsmen. The Economic Times

Improved Policyholder Protections & Transparency

IRDAI is pushing for simpler, clear policy wordings so policyholders better understand what they buy. PayBima+1

New guidelines limit insurers’ ability to repudiate claims on the grounds of non-disclosure or incomplete info for long durations; reduction of moratorium periods in health policies (e.g. from 7 to 5 years) for certain undisclosed conditions unless fraud is involved. PayBima+1

Changes to taxation of certain investment-linked insurance-ULIPs for high premium amounts are in discussion. Grant Thornton Bharat

Governance & Data Regulations

IRDAI has consolidated data maintenance and sharing rules into regulations like IRDAI (Maintenance of Information by Regulated Entities and Sharing of Information), 2025. These require insurers to maintain electronic records, ensure data privacy/security, and use India-based data centers. Insurance Asia

Meeting regulations have been updated to improve efficiency (e.g., virtual meetings allowed, shorter notice for urgent meetings etc.). JSA+1

Impacts for Policyholders

What do these reforms mean for you, as a policyholder or someone considering insurance?

Faster & clearer claims and grievance redressal: Internal ombudsmen should reduce lag time for resolving complaints. Clearer policy wording helps reduce misunderstandings.

More protection for long-term policyholders: Reduced ability for insurers to dispute claims many years later for non-disclosure is helpful.

Possibility of better pricing: GST rationalisation & better regulatory oversight could reduce costs or at least make cost structures of premiums more transparent.

Greater foreign investment & competition: If FDI caps are increased and laws modernised, more players may enter the market, potentially leading to more product choice and competitive pricing.

Better data & privacy safeguards: With stricter requirements for data governance and storage, policyholders’ personal and claim data may be safer.

Things to Watch Out For

While reforms are mostly positive, policyholders should also keep alert on the following:

Even with GST exemptions, insurers losing input tax credits might raise premiums elsewhere (service or admin fee etc.).

Internal ombudsman system is in draft; implementation may take time and vary among companies.

With more regulatory changes, there may be transitional issues—existing policies might need to adapt, or certain policy features/riders may change.

Product changes (ULIPs, health cover) could bring changes in how claims, benefits, or tax treatment work.

How to Benefit / What You Should Do

Here are some tips for policyholders to make the most of these reforms:

Review your policy wordings: After renewals, check the updated policy document for any changes in wording, exclusions, or moratorium period.

Raise grievances if needed: If your insurer isn’t responsive, make use of the grievance mechanism, and later internal ombudsman once companies have appointed them.

Watch for tax changes: Updates in ULIP taxation or GST impact may affect policy costs or returns—consult a financial advisor before making large commitments.

Compare products carefully: As competition and product features evolve, don’t stick to an old policy without checking newer options.

Keep records updated: Since IRDAI is tightening data and disclosure norms, ensure that your personal details, health disclosures etc. are accurate, to avoid trouble during claims.

Conclusion

The IRDAI reforms of 2025 are shaping up to make the Indian insurance market more policyholder-friendly, transparent, and competitive. For clients using platforms like KaroInsure, these changes mean better access, clearer policies, stronger protection, and more options. If you’re an existing policyholder or soon plan to buy insurance,then it’s a good time to review your coverage, stay informed, and ensure your policy aligns with the new regulatory environment.

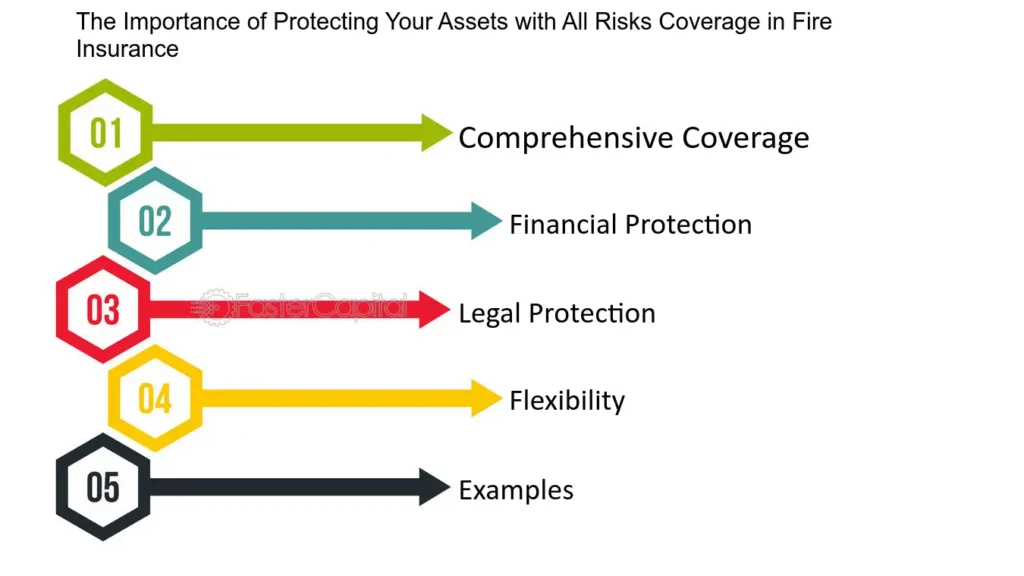

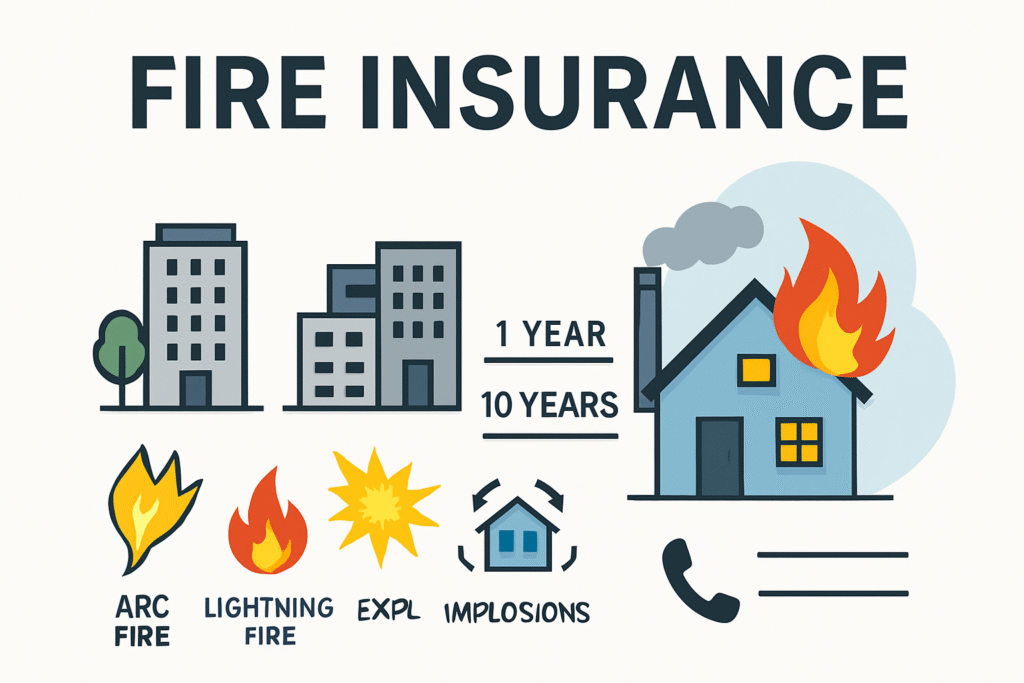

Fire accidents can cause sudden and massive destruction to homes, shops, warehouses, and factories across India. In a country where fire hazards are frequent due to electrical issues, industrial risks, or natural causes, having the right coverage becomes crucial. To ensure safety, individuals and businesses must be aware of the advantages of fire insurance. Through its platform, KaroInsure helps Indian clients access IRDAI-approved fire insurance policies, ensuring protection for residential, commercial, industrial, and agricultural assets.

Fire insurance is a type of property insurance that provides financial compensation for damages or losses caused by fire and related perils. It is based on principles such as indemnity, insurable interest, and utmost good faith. The advantages of fire insurance extend beyond just financial protection, offering peace of mind and long-term stability. KaroInsure connects clients with policies that are transparent, reliable, and tailored to their needs.

Financial Protection Against Fire Losses

One of the primary advantages of fire insurance is financial protection. Fire insurance ensures that the insured is compensated for the actual losses caused by fire, helping individuals and businesses recover quickly.

Homeowners can secure compensation for damaged property and belongings.

Business owners can protect commercial establishments, warehouses, and stock-in-trade.

Industrial units can safeguard expensive machinery and raw materials.

KaroInsure assists Indian clients in choosing policies that provide the right financial safety net.

Business Continuity and Stability

For businesses in India, one of the most crucial advantages of fire insurance is ensuring continuity of operations. Fires can lead to major disruptions, but insurance minimizes downtime by covering asset losses and, in some cases, business interruption.

Small shops and startups benefit from quick recovery support.

Large factories can restart production without heavy financial burden.

Service providers can safeguard office infrastructure.

KaroInsure helps entrepreneurs and enterprises identify policies that include add-ons like business interruption cover for better security.

Peace of Mind for Families and Owners

Peace of mind is among the intangible but significant advantages of fire insurance. Knowing that property and valuables are protected helps Indian families and business owners focus on their lives and operations without constant worry about fire hazards.

KaroInsure ensures this peace of mind by providing easy comparisons and guiding clients through the policy selection process.

Wide Coverage Options

Another key benefit is the wide range of coverage. The advantages of fire insurance include flexibility to insure different types of properties and assets:

Residential Coverage: Houses, flats, furniture, and personal belongings

Commercial Coverage: Shops, offices, and stock-in-trade

Industrial Coverage: Factories, machinery, raw materials, and equipment

Agricultural Coverage: Farmhouses, barns, and produce storage

Through KaroInsure, Indian clients can customize coverage with add-ons like loss of rent, debris removal, and alternate accommodation.

Compliance with Lenders and Regulations

Many financial institutions in India require borrowers to have fire insurance when taking loans against property, factories, or warehouses. Thus, one of the indirect advantages of fire insurance is fulfilling compliance with lenders and regulatory authorities.

KaroInsure simplifies this process by helping clients select the right policy to meet these requirements.

Claim Benefits and Quick Recovery

The ability to file claims and recover losses is one of the most practical advantages of fire insurance. The process ensures:

Immediate reporting of fire incidents

Surveyor assessment of damages

Submission of documents like fire brigade and police reports

Settlement of claims based on actual loss

KaroInsure supports clients during the claim process, making recovery smoother and faster.

Cost-Effective Protection

Another important factor is affordability. The advantages of fire insurance include providing comprehensive protection at relatively low premiums compared to the value of assets insured.

Homeowners can insure property for a nominal yearly premium.

Businesses can cover large inventories at affordable rates.

Industries can secure expensive machinery with flexible options.

KaroInsure helps clients compare multiple insurers to find the most cost-effective plans.

Contribution to Risk Management

Fire insurance also contributes to overall risk management for businesses and individuals. Among the advantages of fire insurance, it encourages responsible behavior by making policyholders adopt safety measures like fire extinguishers, alarms, and preventive maintenance.

This not only reduces the likelihood of incidents but also strengthens claim settlement chances.

Exclusions to Remember

While the advantages of fire insurance are extensive, clients should also know about exclusions. Most policies do not cover:

Damage due to war or nuclear risks

Fires caused intentionally or by gross negligence

Gradual wear and tear of property

Loss of cash, jewelry, or valuables unless specified

KaroInsure guides clients carefully through these exclusions to avoid confusion later.

Why Choose KaroInsure

The advantages of fire insurance become more meaningful when clients choose the right platform. KaroInsure offers:

Access to multiple IRDAI-approved insurers

Transparent comparison of policies

Expert guidance for choosing coverage and add-ons

Support during claims for smoother recovery

With KaroInsure, Indian clients gain not only financial protection but also trusted service and peace of mind.

Conclusion

In conclusion, the advantages of fire insurance include financial protection, business continuity, peace of mind, wide coverage, affordability, and compliance benefits. For Indian individuals, families, and businesses, fire insurance is not just an option but a necessity in today’s uncertain environment. Through its reliable platform, KaroInsure helps clients explore the advantages of fire insurance, compare policies, and secure the best coverage for their needs. By doing so, KaroInsure ensures that valuable assets are protected, risks are minimized, and recovery is made easier after unexpected fire incidents.

Fires can cause devastating losses to homes, shops, offices, warehouses, and factories across India. To safeguard against such risks, individuals and businesses must understand the nature and scope of fire insurance. Through its platform, KaroInsure connects Indian clients with IRDAI-approved fire insurance policies from leading insurers, ensuring protection for residential, commercial, industrial, and agricultural assets.

Understanding Fire Insurance

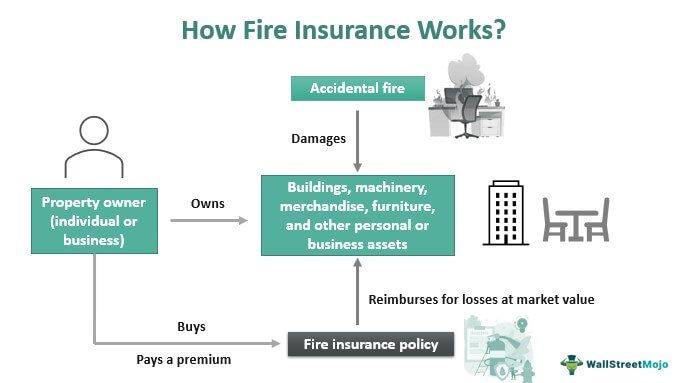

Fire insurance is a form of property insurance designed to provide financial compensation in the event of damage or destruction caused by fire. The nature and scope of fire insurance make it one of the most important risk management tools for Indian households and businesses. It ensures that the insured is indemnified for the actual loss sustained, without enabling profit from the event.

Nature and Scope of Fire Insurance — The Nature of Fire Insurance

When analyzing the nature and scope of fire insurance, it is important to first understand its core characteristics.

Contract of Indemnity: Fire insurance is based on the principle of indemnity, which ensures that the insured is compensated only for the actual loss suffered.

Conditional Contract: The policy is valid only if the insured abides by the terms and conditions, such as timely premium payment and truthful disclosure.

Personal Contract: Fire insurance is a contract between the insurer and the insured. If the ownership of the property changes, the contract does not automatically transfer.

Contract of Utmost Good Faith: Both parties must disclose all material facts honestly. Misrepresentation can result in claim denial.

Insurable Interest: The insured must have a legal or financial interest in the property at the time of both taking the policy and at the time of loss.

These elements define the nature of fire insurance, making it a fair and protective agreement rather than a profit-making tool.

The Scope of Coverage

The scope of fire insurance determines what risks and assets can be covered under the policy. In India, the scope includes:

Residential Property: Coverage for homes, flats, and household contents.

Commercial Property: Shops, offices, warehouses, and stock-in-trade.

Industrial Property: Factories, plants, machinery, and raw materials.

Agricultural Assets: Farmhouses, produce storage, and agricultural equipment.

Special Coverage: Add-ons like earthquake, explosion, lightning, riots, strikes, and malicious damage.

Through KaroInsure, Indian clients can evaluate different insurers and customize the scope of their fire insurance according to their needs.

Exclusions

While understanding the nature and scope of fire insurance, it is equally important to know what is excluded. Common exclusions include:

Damage caused by war, invasion, or nuclear risks

Fire resulting from negligence or deliberate actions

Gradual wear and tear of property

Loss of valuable items like cash, jewelry, or documents unless specifically insured

KaroInsure ensures that clients are fully aware of exclusions so that expectations are managed before purchasing a policy.

Importance for Indian Clients

The nature and scope of fire insurance highlight its critical role in financial protection for Indian households and businesses. Its importance lies in:

Asset Protection: Safeguarding valuable assets from fire-related risks.

Business Continuity: Preventing disruption to operations after fire incidents.

Peace of Mind: Offering security to families and business owners.

Regulatory Compliance: Many businesses are required by lenders or regulators to hold valid fire insurance.

KaroInsure provides easy access to reliable policies, ensuring Indian clients benefit from affordable and adequate protection.

Claim Process in India

A key part of the nature and scope of fire insurance is how claims are settled. The standard claim process in India includes:

Notify the insurer immediately after a fire incident

File a detailed report of damages with supporting documents

Submit fire brigade and police reports, if applicable

Allow surveyors appointed by the insurer to assess losses

Receive compensation based on the principle of indemnity

KaroInsure supports its clients throughout the claim process, making it efficient and transparent.

Add-On Options

The scope of fire insurance can be expanded with add-ons, giving clients extra protection. Popular add-ons in India include:

Loss of Rent: Compensation if the insured property becomes uninhabitable.

Debris Removal: Coverage for the cost of clearing damaged property.

Alternative Accommodation: Temporary housing expenses for families.

Business Interruption Cover: Compensation for loss of income after fire-related damages.

KaroInsure helps Indian clients evaluate and select these add-ons to maximize coverage benefits.

Tips for Indian Clients

To make the most of the nature and scope of fire insurance, Indian clients should:

Assess the correct value of assets before buying insurance

Avoid under-insurance or over-insurance

Disclose all material facts honestly

Compare multiple insurers through KaroInsure before finalizing

Maintain updated documentation for claims

These steps ensure smoother claim settlement and adequate financial protection.

Conclusion

In conclusion, the nature and scope of fire insurance cover its legal principles, coverage area, exclusions, and importance in protecting assets. Fire insurance is a vital tool for Indian individuals, homeowners, and businesses, ensuring financial stability in case of fire-related incidents. Through its trusted platform, KaroInsure connects Indian clients with leading insurers, helping them understand the nature and scope of fire insurance, select the right policy, and manage claims efficiently. By doing so, KaroInsure ensures that clients safeguard their property and achieve peace of mind in an uncertain world.

Fires can cause devastating damage to homes, offices, factories, and warehouses across India. To protect property and minimize financial losses, it is essential to understand the principles of fire insurance. Through its platform, KaroInsure helps Indian clients access IRDAI-approved fire insurance policies, ensuring coverage for residential, commercial, industrial, and agricultural assets while adhering to fundamental insurance principles.

Principles of Fire Insurance — Understanding the Basics

Fire insurance is a type of property insurance that provides financial protection against losses caused by fire, lightning, explosions, or related events. The principles of fire insurance are the foundation upon which all fire insurance policies are designed and executed. By following these principles, Indian clients can make informed decisions when purchasing fire insurance through KaroInsure’s trusted partner network.

Principles of Fire Insurance — Principle of Utmost Good Faith

One of the key principles of fire insurance is the principle of utmost good faith. Both the insurer and the insured must disclose all material facts truthfully. Non-disclosure or misrepresentation can lead to denial of claims.

Indian clients purchasing fire insurance through KaroInsure are guided to provide accurate information about property, assets, and risk factors.

Insurers rely on this principle to assess premiums and policy terms accurately.

Principles of Fire Insurance — Principle of Insurable Interest

The principle of insurable interest ensures that the policyholder has a legal or financial interest in the property being insured. Without insurable interest, a fire insurance policy is not valid.

For Indian businesses, this includes ownership of buildings, machinery, stock, or equipment.

Homeowners must have ownership or legal interest in their residence and contents.

KaroInsure ensures that clients meet the insurable interest requirement before policy issuance.

Principles of Fire Insurance — Principle of Indemnity

The principle of indemnity is central to fire insurance. It states that the insured should not profit from a loss but should be restored to the same financial position as before the loss.

Compensation is limited to the actual loss incurred.

This principle prevents moral hazard and over-insurance.

Through KaroInsure, Indian clients receive policies where indemnity is clearly defined for assets such as residential property, commercial buildings, or industrial equipment.

Principles of Fire Insurance — Principle of Subrogation

The principle of subrogation allows the insurer to take legal action against a third party responsible for the loss, after compensating the insured.

For instance, if a fire in an Indian factory is caused by a neighboring property, the insurer may recover costs from the responsible party.

KaroInsure explains this principle to clients, ensuring clarity about their rights and the insurer’s rights.

Principles of Fire Insurance — Principle of Contribution

If multiple policies cover the same asset, the principle of contribution ensures that the insured cannot claim full compensation from each insurer.

This prevents over-compensation and ensures fairness among insurers.

KaroInsure helps Indian clients coordinate multiple policies, such as residential fire insurance combined with commercial coverage, to avoid conflicts during claims.

Types of Assets Covered

Understanding the principles of fire insurance also involves knowing which assets can be insured. Common assets covered in India include:

Residential Property: House structure, furniture, electrical fittings, and personal belongings

Commercial Property: Offices, shops, stock-in-trade, and office equipment

Industrial Property: Factories, machinery, raw materials, and finished goods

Agricultural Assets: Farmhouses, storage sheds, crop stock, and farm equipment

KaroInsure guides clients in selecting policies that match the type and value of assets, ensuring adequate protection.

Importance for Indian Clients

Adhering to the principles of fire insurance is crucial for Indian clients because it:

Protects assets and minimizes financial losses due to fire accidents

Ensures compliance with IRDAI regulations and policy terms

Prevents disputes and denial of claims due to non-disclosure or misrepresentation

Promotes responsible insurance practices for businesses and homeowners

KaroInsure ensures that clients are aware of these principles and follow them when purchasing policies.

Claim Process in India

A smooth claim process depends on understanding the principles of fire insurance:

Notify the insurer immediately after the fire incident

Submit a detailed list of damaged assets along with fire brigade or police reports

Provide documentation that confirms insurable interest and property value

Allow the insurer’s surveyor to assess the damage

Receive settlement based on actual loss under the principle of indemnity

KaroInsure supports Indian clients throughout the claims process, making it transparent and efficient.

Tips for Indian Clients

To maximize benefits, Indian clients should:

Ensure complete and accurate disclosure of assets and risks

Verify insurable interest before purchasing a policy

Avoid over-insurance to comply with the principle of indemnity

Understand exclusions, add-ons, and limits of coverage

Maintain documentation for easy claim settlement

KaroInsure provides guidance and comparison tools, ensuring clients select policies that adhere to principles of fire insurance while meeting coverage needs.

Conclusion

In conclusion, the principles of fire insurance — utmost good faith, insurable interest, indemnity, subrogation, and contribution — form the foundation of effective fire insurance policies. Understanding these principles helps Indian homeowners, businesses, and industrial clients select IRDAI-approved policies that protect residential, commercial, industrial, and agricultural assets. Through KaroInsure, clients gain access to trusted insurers, clear guidance on coverage, and support throughout the claim process, making fire insurance simple, reliable, and fully compliant with regulatory standards in India.

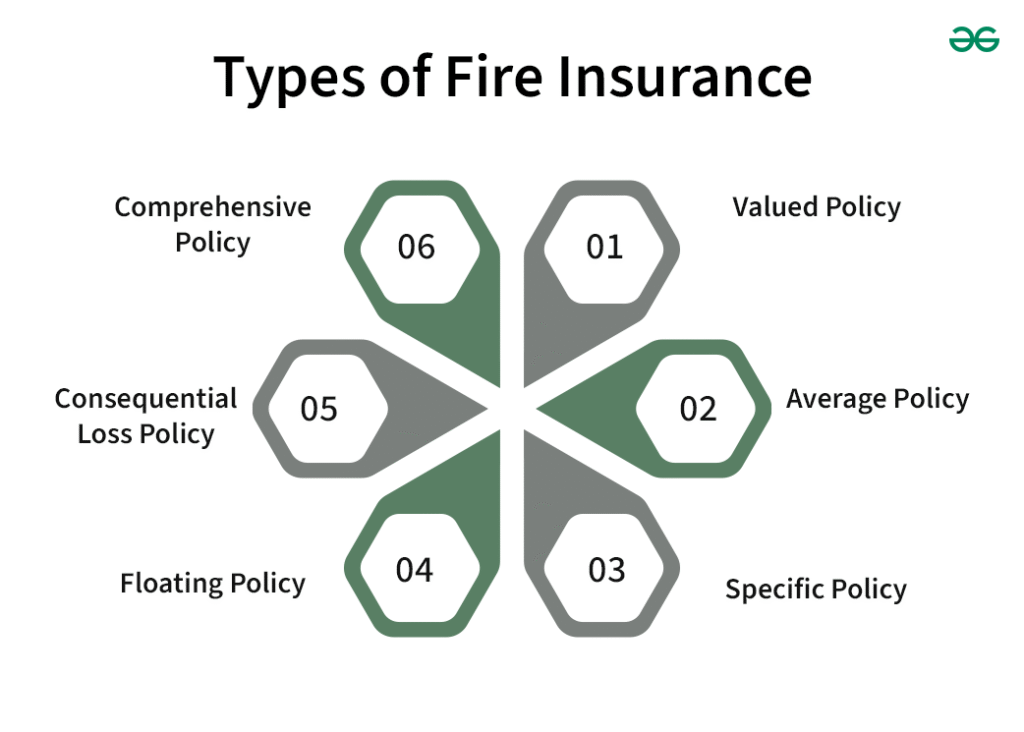

Fires can cause significant damage to homes, offices, factories, and warehouses in India. To mitigate financial losses, it is essential for individuals and businesses to understand the types of fire insurance policy available. Through its platform, KaroInsure helps Indian clients explore and purchase fire insurance policies from trusted partner insurers, providing coverage for residential, commercial, industrial, and agricultural assets.

Understanding Fire Insurance

Fire insurance is a type of property insurance that provides financial protection against damage caused by fire, lightning, explosion, or implosion. Knowing the types of fire insurance policy helps Indian clients select the most suitable coverage based on the nature of their property and assets. KaroInsure ensures access to IRDAI-approved policies, providing clarity on coverage, exclusions, and benefits.

Standard Fire Insurance Policy

The most common option among the types of fire insurance policy is the standard fire insurance policy. It covers:

Residential property, including walls, roof, and permanent fixtures

Commercial property like shops, offices, and showrooms

Damage caused by fire, lightning, and explosions

Certain natural events, depending on policy terms

This policy is ideal for homeowners and small businesses seeking basic fire protection. KaroInsure guides clients in comparing premiums and selecting the best standard policy.

Industrial Fire Insurance Policy

For factories and large-scale operations, industrial assets require specialized coverage. The types of fire insurance policy in this category include:

Coverage for factory buildings, warehouses, and production units

Protection for machinery, boilers, and equipment

Stock of raw materials, semi-finished goods, and finished products

Additional protection for fire caused by electrical faults or industrial hazards

Through KaroInsure, Indian industrial clients can choose policies tailored to their operations and equipment value.

Commercial Fire Insurance Policy

Small and medium businesses in India often opt for commercial fire insurance. Among the types of fire insurance policy, commercial coverage typically includes:

Office buildings, shops, and showrooms

Furniture, fixtures, and office equipment

Stock-in-trade and merchandise

Optional add-ons like loss of rent or business interruption cover

KaroInsure helps business owners compare and select commercial policies, ensuring comprehensive asset protection.

Home or Residential Fire Insurance

Residential clients in India also benefit from understanding the types of fire insurance policy. Home fire insurance generally covers:

House structure, including walls, floors, and roof

Electrical installations, built-in furniture, and kitchen fittings

Household goods, furniture, and appliances

Optional add-ons for valuables, personal effects, or natural disaster coverage

KaroInsure simplifies the process for homeowners, providing access to policies that suit property type and asset value.

Agricultural Fire Insurance Policy

Agricultural properties face unique fire risks due to flammable materials and farm activities. The types of fire insurance policy for agricultural assets include:

Farmhouses, storage sheds, and barns

Crop storage and produce in warehouses

Agricultural machinery and tools

Coverage for fire caused by natural events like lightning

Through KaroInsure, farmers and agricultural businesses in India can secure specialized fire insurance tailored to their operational risks.

Add-On Coverage Options

Beyond the basic types, many fire insurance policies offer add-ons to enhance protection. These include:

Loss of Rent: Covers rental income lost due to fire damage

Debris Removal: Costs to clear damaged property after a fire

Alternate Accommodation: Temporary housing for affected families

Explosion and Implosion: Coverage for damage from sudden blasts

Riot, Strike, and Malicious Damage: Extends protection to fires caused by social unrest

KaroInsure helps Indian clients customize policies with these add-ons for complete coverage.

Exclusions to Know

When considering the types of fire insurance policy, it is important to understand what is not covered:

Losses due to war, invasion, or nuclear risks

Fire caused by negligence or intentional acts

Damage to cash, jewelry, or precious documents unless specified

Wear and tear or gradual deterioration of property

KaroInsure guides clients in reviewing exclusions, ensuring policies meet expectations without surprises during claims.

Claim Process in India

Understanding the claim process is essential for any fire insurance policy. Indian clients using types of fire insurance policy can follow these steps:

Notify the insurer immediately after the fire incident

Submit documentation, including fire brigade and police reports

Provide an inventory of damaged assets and supporting documents

Allow insurer surveyor to assess losses

Receive settlement based on verified damages

KaroInsure assists clients throughout the claims process, making it easier to recover losses quickly and efficiently.

Importance for Indian Clients

Awareness of the types of fire insurance policy is crucial for Indian homeowners, businesses, and industrial units. Proper coverage ensures:

Protection of valuable assets from financial loss

Peace of mind and security for families and employees

Continuity of business operations after fire-related incidents

Compliance with IRDAI regulations for insurance

KaroInsure connects clients with trusted insurers, providing policies that are transparent, reliable, and suitable for different asset types.

Conclusion

In conclusion, the types of fire insurance policy available in India include standard fire, industrial, commercial, residential, and agricultural policies. Each type offers coverage tailored to the specific needs of property and assets. By partnering with IRDAI-approved insurers, KaroInsure helps Indian clients select the right fire insurance policy, customize coverage with add-ons, and navigate claims efficiently. Understanding and investing in the right type of fire insurance policy ensures financial protection, operational stability, and peace of mind for individuals and businesses across India.

Fires can cause devastating losses to homes, offices, factories, and shops. In India, where small and medium-sized businesses often operate with limited backup resources, fire-related accidents can result in financial ruin. This is where fire insurance comes in. Many business owners and individuals ask the common question: fire insurance provides cover for which assets? Through its platform, KaroInsure helps Indian clients understand and purchase fire insurance policies from trusted partner insurers, ensuring that valuable assets are adequately protected against unforeseen fire risks.

Understanding the Basics

Before diving into specific assets, it’s important to understand the purpose of fire insurance. A fire insurance policy is designed to provide compensation for damages caused by fire and related risks such as lightning, explosion, or implosion. Knowing exactly fire insurance provides cover for which assets helps policyholders make informed decisions when selecting a policy. KaroInsure ensures that its Indian clients get access to IRDAI-approved fire insurance policies that clearly outline the scope of coverage.

Residential Property

One of the primary answers to fire insurance provides cover for which assets is residential property. Homeowners can insure their houses against fire damage, including:

The building structure (walls, roof, floors)

Electrical fittings and fixtures

Built-in wardrobes, kitchen cabinets, and other permanent fittings

Personal belongings such as furniture, appliances, and electronics

KaroInsure helps Indian homeowners compare different fire insurance options to protect their homes, ensuring complete coverage and peace of mind.

Commercial Property

Businesses in India must consider what fire insurance provides cover for which assets in their commercial spaces. Coverage typically includes:

Office buildings, shops, or showrooms

Furniture, fixtures, and fittings inside the workplace

Computers, servers, and office equipment

Raw materials and finished stock stored in warehouses or retail outlets

Through KaroInsure, Indian business owners can choose commercial fire insurance policies that safeguard their assets against financial loss from fire-related incidents.

Industrial Property

Industrial setups are often at a higher risk of fire due to machinery, flammable materials, and large-scale operations. In this case, fire insurance provides cover for which assets includes:

Factories and manufacturing units

Heavy machinery and production equipment

Boilers, turbines, and industrial tools

Stock of raw materials, semi-finished goods, and finished products

KaroInsure works with partner insurers who offer specialized fire insurance plans for industrial clients, ensuring coverage for both property and equipment.

Agricultural and Farm Assets

In rural India, farmers and agricultural businesses also need protection against fire. When asking fire insurance provides cover for which assets, the answer extends to:

Farmhouses and storage sheds

Agricultural produce stored in warehouses

Farm machinery and equipment

Stock of seeds, fertilizers, and pesticides

By connecting with KaroInsure, agricultural businesses can explore fire insurance options designed to safeguard rural and farm-based assets.

Valuable Goods and Stock

Many small businesses in India depend heavily on inventory. For them, fire insurance provides cover for which assets such as:

Retail goods stored in shops or warehouses

Stock-in-trade for wholesalers and distributors

Perishable goods, if covered under specific fire insurance clauses

Merchandise awaiting shipment or delivery

KaroInsure ensures small and medium-sized businesses get access to fire insurance that adequately covers their stock, helping them avoid devastating losses.

Add-On Coverages

Apart from standard coverage, fire insurance provides cover for which assets can extend further with add-ons, such as:

Loss of Rent: Covers rental income lost due to fire damage

Debris Removal: Costs involved in clearing the site after a fire

Alternate Accommodation: Temporary housing for families affected by fire

Explosion and Implosion: Covers damages caused by sudden blasts

Riot, Strike, and Malicious Damage: Extends protection to fire caused by social unrest

KaroInsure assists Indian clients in customizing their fire insurance policies with such add-ons for complete protection.

Exclusions to Note

While discussing fire insurance provides cover for which assets, it is equally important to know what is not covered:

Losses caused by war, invasion, or nuclear risks

Fire damage due to willful negligence or misconduct

Loss of valuables like cash, jewelry, or precious documents unless specifically covered

Wear and tear or gradual deterioration of assets

KaroInsure helps Indian clients understand these exclusions before purchasing policies, ensuring there are no surprises at the time of claims.

Claim Process in India

To claim under fire insurance, Indian clients must follow a structured process:

Notify the insurer immediately after the fire incident

Provide details of the damaged property and assets

Submit fire brigade reports, police reports, and other documents

Allow a surveyor appointed by the insurer to assess the loss

Receive claim settlement after verification

Through KaroInsure’s support, Indian policyholders can navigate the fire insurance claim process smoothly and efficiently.

Importance for Indian Businesses and Individuals

Understanding fire insurance provides cover for which assets is crucial for both businesses and households in India. For businesses, it ensures financial security and operational continuity. For homeowners, it provides peace of mind and protection against unexpected losses. KaroInsure’s platform simplifies the process by connecting clients with trusted insurers, ensuring access to policies that are transparent, affordable, and IRDAI-compliant.

Conclusion

In conclusion, the answer to fire insurance provides cover for which assets includes residential property, commercial and industrial property, agricultural assets, stock, machinery, and more. Fire insurance plays a vital role in protecting valuable assets from unforeseen disasters. By partnering with trusted insurers, KaroInsure enables Indian clients to purchase the right fire insurance policies, ensuring complete protection for homes, businesses, and industries. With digital convenience and expert guidance, KaroInsure makes fire insurance simple, transparent, and reliable.