In a rapidly growing economy like India, lending plays a crucial role in business expansion and personal finance. Banks, NBFCs, and microfinance institutions provide billions in loans every year to individuals and businesses. However, lending always carries one major risk—default. When a borrower fails to repay, lenders face serious financial losses.

To protect against such risks, a modern solution called credit default insurance in India is gaining popularity. This insurance acts as a financial safety net for lenders while maintaining confidence in India’s credit system.

What Is Credit Default Insurance?

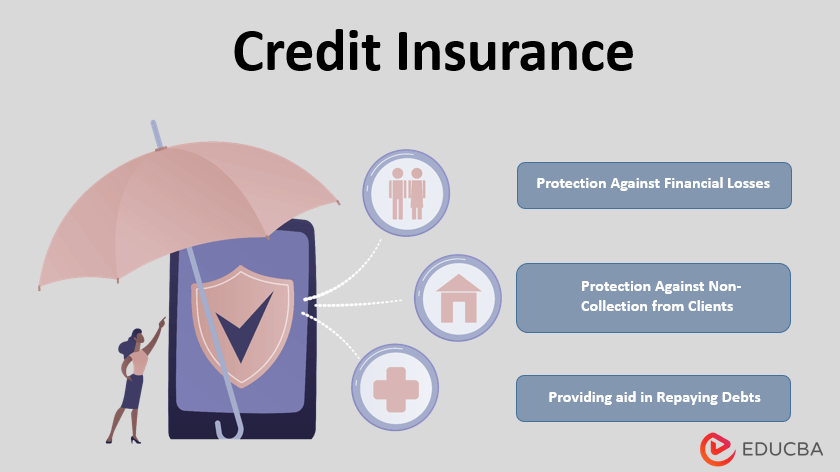

Credit default insurance (CDI) is a policy that protects lenders or investors from losses if borrowers fail to repay their debts. It works like a guarantee — if the borrower defaults, the insurer compensates the lender for part or all of the outstanding loan amount.

In simpler terms, credit default insurance in India ensures that lenders don’t suffer heavy losses even when loans go bad. This is particularly useful for institutions with large credit portfolios, such as banks, NBFCs, and fintech lending firms.

How Does Credit Default Insurance Work?

The process is straightforward:

- The lender purchases a policy covering specific loans or a portfolio of loans.

- The insurer evaluates risk based on borrower profiles, credit history, and market factors.

- Premiums are paid according to the coverage amount and assessed risk.

- If a borrower defaults, the insurer reimburses the lender, usually covering 75%–90% of the unpaid amount.

This arrangement allows lenders to continue extending credit confidently, knowing they are financially protected.

Why Credit Default Insurance Matters in India

India’s credit sector has seen tremendous growth, but also rising loan defaults, especially after economic disruptions like the pandemic. For lenders, even a small default rate can impact profitability.

Here’s why credit default insurance in India has become vital:

- Risk Management: Helps financial institutions balance risk across diverse borrower profiles.

- Encourages Lending: Insured lenders are more likely to approve loans for startups, MSMEs, and individuals with limited credit history.

- Investor Confidence: Reduces uncertainty for investors backing lending institutions.

- Regulatory Compliance: Insurance coverage can support asset quality requirements set by regulators.

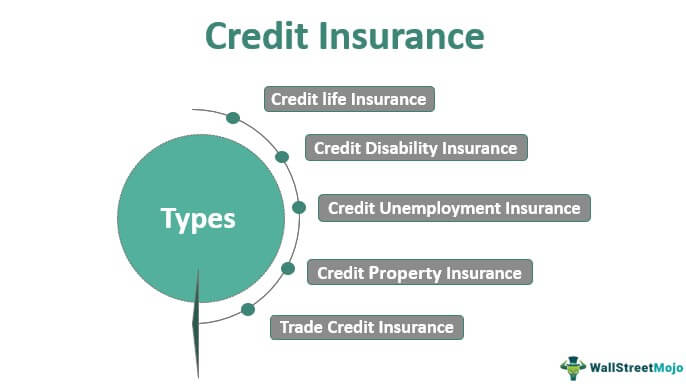

Types of Credit Default Insurance

Different forms of credit default insurance cater to specific market needs:

1. Individual Loan Default Insurance

Covers a specific borrower’s loan, such as a home loan, business loan, or vehicle loan.

2. Portfolio Default Insurance

Protects a group of loans, commonly used by banks and NBFCs for managing collective credit risk.

3. Trade Credit Insurance

Covers businesses against losses from unpaid invoices or non-payment by buyers in B2B transactions.

4. Credit Derivative Insurance (CDS)

Used by institutional investors to hedge against bond or debt default risk.

Each type serves different sectors but shares a common goal—protecting lenders from default losses.

Benefits of Credit Default Insurance in India

For Lenders

- Reduced Financial Exposure: Protects against large-scale losses from borrower defaults.

- Increased Lending Confidence: Encourages credit expansion to high-risk or underserved segments.

- Improved Asset Quality: Insured loans strengthen balance sheets and investor trust.

For Borrowers

- Easier Loan Access: Lenders may offer loans more readily when risks are covered.

- Lower Interest Rates: Reduced risk for lenders can result in competitive interest offers.

- Flexible Terms: Borrowers may gain longer repayment tenures or higher loan limits.

Challenges in Implementing Credit Default Insurance

Despite its advantages, credit default insurance in India faces some practical challenges:

- Limited Awareness: Many small financial institutions and borrowers are unaware of its benefits.

- High Premium Costs: Premiums can be expensive for high-risk sectors or startups.

- Data Limitations: Accurate borrower risk assessment depends on strong data systems, which are still developing in some areas.

- Regulatory Uncertainty: The product category is relatively new, and consistent guidelines are still evolving.

However, as India’s financial ecosystem matures, insurers and regulators are working to make such coverage more accessible and standardized.

The Role of Credit Default Insurance in Strengthening India’s Economy

The rise of credit default insurance in India supports the broader financial infrastructure in multiple ways:

- Encourages Entrepreneurship: Startups and small businesses gain easier access to loans.

- Reduces NPA Burden: Helps banks manage and reduce non-performing assets (NPAs).

- Boosts Investor Trust: Domestic and foreign investors feel more secure in funding Indian lenders.

- Promotes Financial Inclusion: Expands credit access to rural and semi-urban borrowers who lack traditional collateral.

By minimizing default-related risks, this insurance helps sustain India’s credit-driven economic growth.

How to Choose the Right Credit Default Insurance Policy

If you’re a lender or financial institution considering CDI, here are key factors to evaluate:

- Coverage Limit: Check how much of the loan amount is insured—some cover up to 90%.

- Premium Rate: Ensure premiums are proportionate to your risk level and loan volume.

- Claims Process: A quick, transparent process is essential for liquidity protection.

- Reputation of Insurer: Work with trusted insurers experienced in credit risk management.

- Exclusions: Understand conditions under which claims may be denied.

Comparing multiple options through a reliable platform like KaroInsure can help find the most suitable plan.

The Future of Credit Default Insurance in India

With the rapid digitization of lending, the need for risk management tools like CDI will only increase. AI-based credit scoring and fintech partnerships are making loan issuance faster—but they also raise exposure to new forms of default risk.

In the coming years, credit default insurance in India is expected to evolve with:

- Integration into digital lending platforms.

- Flexible micro-insurance products for small-ticket loans.

- Collaboration between banks and insurers for customized coverage.

- Government support to strengthen financial stability and inclusion.

As the Indian lending market grows, CDI will play a key role in ensuring both lenders and borrowers stay financially protected.

Conclusion

In an economy powered by credit, protecting against loan defaults is essential. Credit default insurance in India offers a strong shield for lenders and borrowers alike, ensuring business continuity, financial confidence, and stability.

Whether you are a bank, NBFC, or fintech lender, adopting credit default insurance is not just about protection—it’s about enabling growth with security.

With KaroInsure, financial institutions can easily compare and select the most effective credit default insurance plans, keeping lending operations resilient and future-ready.

Leave a Reply