Healthcare costs in India are rising faster than ever. A single medical emergency can drain years of savings. While most people understand the importance of having a health insurance policy, very few know that it might not be enough in the face of serious diseases like cancer, heart attack, or kidney failure. This is where a Critical Illness Cover steps in.

In this article, we’ll explain the difference between critical illness and standard health insurance in India, how each works, and why combining both can give you complete financial protection.

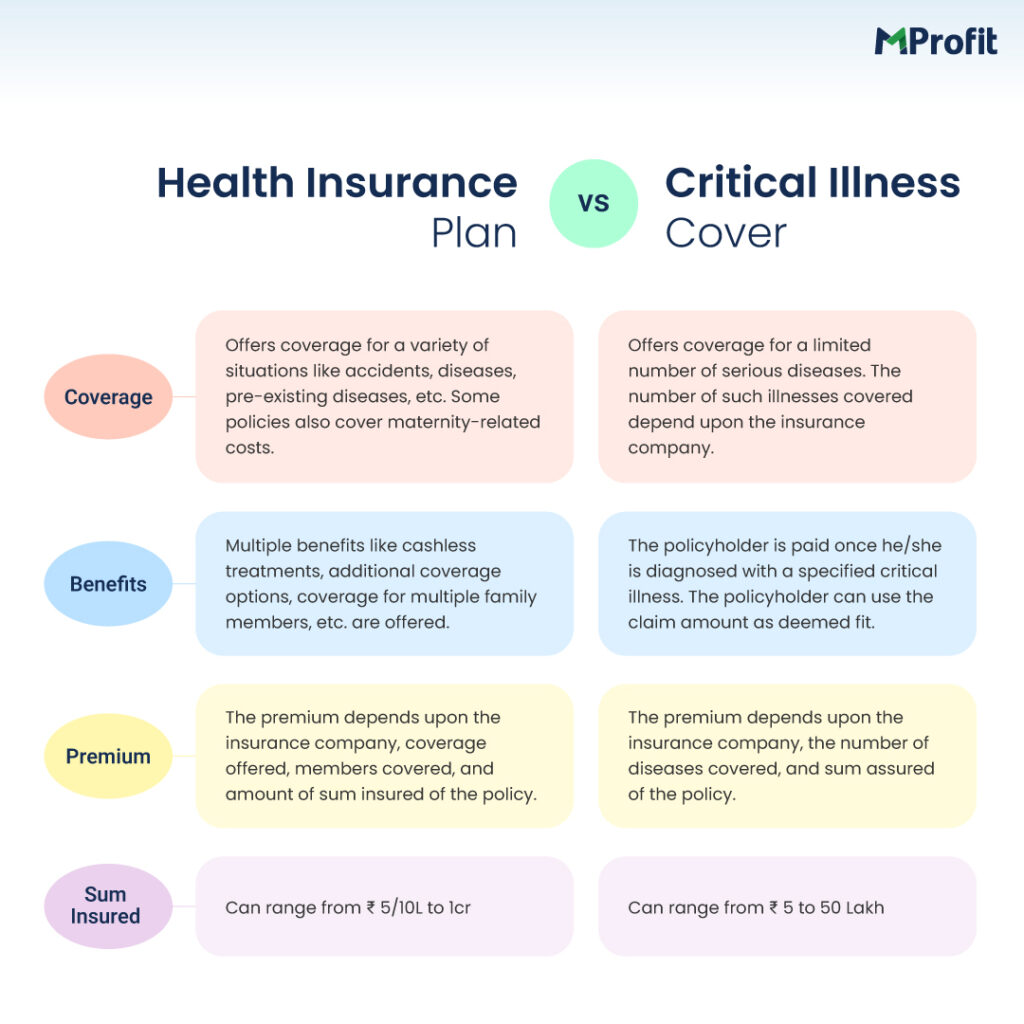

What Is Standard Health Insurance?

A standard health insurance policy covers your medical expenses during hospitalization. It reimburses or directly pays for the costs of:

- Hospital room rent

- Doctor consultations

- Surgery or treatment

- Medicines and diagnostic tests

This type of insurance works on a reimbursement or cashless model. You either pay the bills and claim reimbursement later or use the insurer’s hospital network for direct payment.

Example: If you are hospitalized due to pneumonia, your health insurance will pay your hospital bills up to the sum insured.

However, the moment you recover and are discharged, the coverage ends for that event. You won’t receive any extra money for recovery or loss of income.

What Is Critical Illness Insurance?

A Critical Illness Cover is designed for severe, life-threatening diseases that require long-term treatment or rehabilitation. These include cancer, stroke, heart attack, organ failure, and similar illnesses.

Unlike standard health insurance, it pays a lump-sum amount as soon as the disease is diagnosed — regardless of the actual hospital expenses.

This amount can be used for:

- Medical and non-medical expenses

- Home care or recovery costs

- Paying EMIs or rent during treatment

- Supporting your family financially if you can’t work

Example: If your policy offers ₹10 lakh coverage for critical illnesses and you are diagnosed with cancer, you receive the full ₹10 lakh payout immediately after claim approval — even if your treatment costs ₹5 lakh or ₹15 lakh.

Key Differences: Critical Illness vs. Health Insurance in India

| Feature | Standard Health Insurance | Critical Illness Insurance |

|---|---|---|

| Coverage Type | Hospitalization and medical expenses | Lump-sum payout on diagnosis of a critical disease |

| Claim Basis | Reimbursement or cashless | One-time fixed payment |

| Diseases Covered | All covered conditions requiring hospitalization | Specific critical illnesses listed in policy |

| Purpose | To cover medical treatment costs | To provide income replacement and financial support |

| Premium | Based on age, sum insured, and health condition | Generally lower, depends on coverage and illness list |

| Renewability | Annual renewal | Long-term (often up to age 60 or 65) |

| Waiting Period | 30–90 days for illness coverage | 90 days or more for listed critical illnesses |

Why Critical Illness Cover Is Essential in India

India is witnessing a rapid rise in lifestyle diseases. According to IRDAI and health reports, nearly 60% of all deaths in India are linked to non-communicable diseases like cancer and heart problems.

Even the best hospital insurance may not cover the hidden financial impact — such as income loss, travel for treatment, or long-term care.

A critical illness plan bridges this gap by giving you liquidity and flexibility when you need it the most.

Key benefits:

- Financial Cushion: Provides a tax-free lump sum to use as needed.

- Covers Lifestyle Diseases: Offers protection from high-cost illnesses.

- Works with Health Insurance: Complements your existing policy for total protection.

- Affordable Premiums: Especially cost-effective when bought early in life.

Example: How Both Covers Work Together

Let’s assume Ravi, a 35-year-old professional, has:

- Health Insurance: ₹5 lakh sum insured

- Critical Illness Cover: ₹10 lakh

He is diagnosed with a heart condition requiring surgery. His hospital bills total ₹4 lakh.

- His health insurance pays the ₹4 lakh directly to the hospital.

- His critical illness plan gives him ₹10 lakh as a lump sum.

Ravi uses part of this amount for recovery, family expenses, and post-surgery care — without worrying about income loss.

This combination ensures both medical and financial security, which is essential for long-term peace of mind.

Choosing Between the Two: What Should You Do?

If you are comparing critical illness vs. health insurance in India, the best option is not to choose one over the other, but to combine both.

Here’s why:

- Health insurance handles immediate hospitalization costs.

- Critical illness insurance supports life after diagnosis.

Together, they cover all aspects of health-related financial risk.

How to Choose the Right Critical Illness Cover

When buying a policy, consider:

- Number of Diseases Covered: Check the list carefully; most plans cover 20–40 illnesses.

- Claim Payout Terms: Understand when and how the lump sum is released.

- Waiting and Survival Period: Usually, you must survive 30 days after diagnosis to claim benefits.

- Premium Affordability: Compare costs from multiple insurers.

- Add-on vs. Standalone Policy: You can buy it separately or as a rider to your main plan.

Tax Benefits

Both standard and critical illness policies offer tax deductions under Section 80D of the Income Tax Act. You can claim up to ₹25,000 (₹50,000 for senior citizens) for premiums paid — making these plans even more beneficial.

Conclusion

When it comes to critical illness vs. health insurance in India, both serve distinct but equally important purposes. A standard health plan ensures your hospital bills are taken care of, while a critical illness plan protects your long-term financial stability.

In today’s uncertain health environment, combining the two is the smartest move for complete peace of mind.

Secure your health and finances with KaroInsure — compare top plans and choose the right mix of health and critical illness insurance today.

Leave a Reply